By Charlie Case | Winburn, Case, Schrader & Shram, PLLC | April 2026

Nobody plans to need long-term care. But most of us will — and the cost can be staggering. Here is what Arkansans need to know about long-term care planning: what care costs, how Medicaid works, and what legal tools exist to protect you and your family.

How likely are you to need long-term care?

The risk is higher than most people expect. The U.S. Department of Health and Human Services projects that 56% of people turning 65 will develop a significant disability requiring long-term services and supports. Broader estimates that count any form of care — including informal family assistance — approach 70%. For a healthy couple, there is a 75% chance that at least one spouse will require a significant level of long-term care.

What does long-term care cost in Arkansas?

Arkansas care costs are below the national median — but they are not cheap, and they are rising. According to the 2025 Cost of Care Survey conducted by CareScout, here is what Arkansans can expect to pay:

- Home care (non-medical caregiver): approximately $4,767 per month ($57,200 annually)

- Assisted living: approximately $4,562 per month ($54,744 annually)

- Nursing home, semi-private room: approximately $7,452 per month ($89,425 annually)

- Nursing home, private room: approximately $8,060 per month ($96,725 annually)

For context, the national median for a private nursing home room is $10,798 per month. Arkansas remains more affordable — but costs here continue to climb, with nursing home rates rising 4-5% in 2025 alone.

How do people pay for long-term care?

Medicare does not cover long-term custodial care — the day-to-day help with bathing, dressing, eating, and mobility that most people eventually need. Medicare covers only short-term skilled nursing care following a qualifying hospital stay. For extended care, families typically rely on one or more of three sources.

- Out-of-pocket (private pay)

Many families pay directly from savings and retirement accounts. This approach works until resources run low — which is precisely when the other options become critical. - Long-term care insurance

LTC insurance pays a daily or monthly benefit when you can no longer perform a certain number of activities of daily living, or when you have a qualifying cognitive impairment such as Alzheimer’s disease. Waiting to buy is costly: the same coverage at age 65 runs 50% or more higher than at age 55, and insurers deny nearly half of applicants in their seventies on health grounds.Arkansas participates in the national Long-Term Care Partnership Program. A Partnership-qualified policy creates a direct link to Medicaid: for every dollar the policy pays in benefits, Medicaid will protect that same dollar of assets when evaluating eligibility — dollar for dollar. The asset disregard also applies to estate recovery after death. - Medicaid

Medicaid covers approximately 61% of all long-term care costs nationally. But qualifying requires meeting strict financial rules, and most middle-class Arkansans do not qualify without first spending down most of what they have worked a lifetime to accumulate.

Qualifying for Medicaid long-term care in Arkansas

Arkansas Medicaid long-term care covers nursing home care, assisted living through the LivingChoices Waiver, and in-home care through the ARChoices Waiver. Eligibility requires both a functional need and meeting financial limits that differ significantly depending on whether you are single or married.

Single applicants

- Asset limit: $2,000 in countable assets

- Income limit: $2,982 per month (2026)

- The home, one vehicle, household furnishings, and certain prepaid burial plans are generally exempt

- Patient liability: almost all income above a $40/month personal needs allowance must be paid toward the cost of care

Married applicants (one spouse needing care)

Federal spousal impoverishment rules prevent a well spouse from being left destitute. Under current 2026 Arkansas rules, the community spouse may retain up to $162,660 through the Community Spouse Resource Allowance, or at least $32,532. regardless of the couple’s total. The community spouse’s own income is not restricted — they keep every dollar received in their own name.

Medicaid financial limits are adjusted periodically. The figures above reflect 2025–2026 thresholds. Verify current limits with an elder law attorney or Arkansas DHS before relying on them for planning.

The five-year Medicaid lookback period

Arkansas applies a 60-month lookback period to nursing home and waiver applications. Gifts or transfers for less than fair market value made within five years of application trigger a penalty period of ineligibility. Staying within the IRS annual gift tax exclusion does not protect a transfer from Medicaid scrutiny — the two sets of rules operate independently.

Medicaid estate recovery in Arkansas — the rule families often miss

Qualifying for Medicaid is not the end of the story. Federal law requires every state to seek reimbursement from the estate of a deceased Medicaid recipient for long-term care costs paid on their behalf. In Arkansas, the home is the asset most often at risk.

Arkansas is a “probate-only” recovery state, meaning the state can only pursue assets that pass through probate. A critical Arkansas-specific protection exists: under Act 570 of 2021, the state may not make a Medicaid estate recovery claim against property transferred through a properly executed and recorded beneficiary deed. The owner retains full control during their lifetime, can revoke the deed at any time, and the deed does not trigger the five-year lookback period.

The beneficiary deed’s protection applies to real property only. Other assets require separate planning.

Asset protection strategies for long-term care planning

The law provides meaningful tools to manage long-term care costs and protect assets for the next generation. Which tools are available — and how effective — depends almost entirely on when planning begins.

Medicaid Asset Protection Trusts (MAPTs)

An irrevocable Medicaid Asset Protection Trust holds assets outside of your personal ownership for Medicaid purposes. Once properly funded, those assets are generally not counted toward the Medicaid asset limit and are protected from estate recovery. The trust must be funded at least five years before applying for Medicaid. A revocable living trust does not provide this protection.

The Arkansas beneficiary deed

Even without a MAPT, the beneficiary deed is a powerful and low-cost tool for protecting the family home from estate recovery. A properly executed and recorded deed can preserve the home for heirs without probate, without triggering the lookback, and without surrendering lifetime control.

Powers of attorney

Every financial and legal strategy described in this post requires someone with legal authority to act on your behalf. If you become incapacitated without valid powers of attorney in place, that authority does not automatically transfer to your spouse or children. Your family may be forced to seek a court-supervised guardianship or conservatorship — a process that is public, costly, time-consuming, and entirely avoidable with advance planning.

Two paths: what you can protect depends on when you plan

Every family that ends up in crisis planning wished they had planned earlier. Not because crisis planning fails — it can be genuinely helpful — but because the tools available in a crisis are a fraction of what is available when you have time.

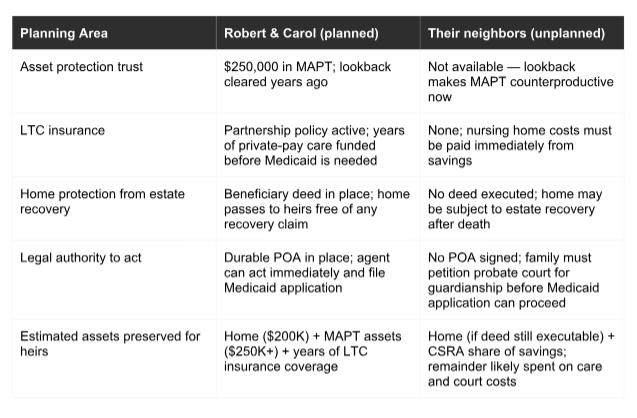

The following is a hypothetical illustration for educational purposes only. It does not represent any actual client or situation. Outcomes in individual cases will vary based on specific facts, applicable law, and the advice of a qualified attorney.

Consider two fictional Arkansas couples, Robert and Carol, and their neighbors. Both couples are in their early 60s with similar finances: a paid-off home worth $200,000, $300,000 in savings and retirement accounts, and modest monthly income. Eight years later, one spouse in each couple requires nursing home care.

Robert and Carol met with an elder law attorney years earlier. They funded a Medicaid Asset Protection Trust with $250,000 in savings, purchased a Partnership-qualified LTC insurance policy, executed beneficiary deeds on their home, and signed durable powers of attorney. The five-year lookback cleared years ago.

Their neighbors intended to plan but never got around to it. When the care need arrives, there is no trust, no LTC insurance, and no power of attorney — and the ill spouse has already lost the capacity to sign documents.

Robert and Carol’s neighbors still have options. Spousal impoverishment rules allow the community spouse to retain the CSRA share of assets. A beneficiary deed can still be executed — if the ill spouse retains capacity to sign. These are real tools that can make a meaningful difference. But the $250,000 in the MAPT is out of reach, the LTC insurance that would have covered years of private-pay care was never purchased, and the family must navigate a guardianship proceeding before anyone can even apply for Medicaid. Crisis planning is skilled triage. Long-term planning is the plan.

Talk to an Arkansas elder law attorney

Long-term care is a near-certainty for most Arkansas families. The costs are substantial and rising. Medicare will not cover most of it. Medicaid will, but only after strict financial requirements are met — and even then the state may seek reimbursement from what is left behind.

Real solutions exist at every stage of planning. LTC insurance — especially Partnership-qualified policies — can cover years of care and shield assets from Medicaid spend-down. MAPTs can protect savings and investments given enough lead time. Beneficiary deeds can protect the family home from estate recovery at minimal cost. And well-drafted powers of attorney ensure that every other tool in the plan can actually be used when it is needed most.

For a deeper look at how these rules and tools apply to families with real estate, retirement accounts, and farm assets, read our detailed guide: Long-Term Care Planning and Medicaid in Arkansas — What Families Need to Know Before a Crisis.

Our firm helps Arkansas families navigate all of these options — whether you are planning ahead or responding to an immediate need. Call us at (501) 975-6266 or Contact Us to schedule a consultation.

Frequently Asked Questions

Does Medicare cover nursing home care in Arkansas?

Medicare does not cover long-term custodial nursing home care. It covers only short-term skilled nursing care following a qualifying hospital stay of at least three days, and only for a limited period. Families who need extended nursing home care must pay out of pocket, use long-term care insurance, or qualify for Arkansas Medicaid.

How much does a nursing home cost in Arkansas?

According to the 2025 CareScout Cost of Care Survey, the median cost of a semi-private nursing home room in Arkansas is approximately $7,452 per month ($89,425 annually), and a private room costs approximately $8,060 per month ($96,725 annually). Assisted living costs a median of about $4,562 per month. These figures are below the national median but rose 4-5% in 2025.

What is the five-year Medicaid lookback period in Arkansas?

When you apply for Arkansas Medicaid nursing home coverage, the state reviews all asset transfers — including gifts — made during the five years before your application date. Transfers for less than fair market value can result in a penalty period during which Medicaid will not pay for care. Giving assets away under the IRS annual gift tax exclusion does not protect those transfers from Medicaid scrutiny.

What assets are protected for a spouse when the other enters a nursing home in Arkansas?

When one spouse applies for Arkansas Medicaid nursing home coverage, the at-home spouse may retain up to $162,660 in assets through the Community Spouse Resource Allowance (2026 figure), or at least $32,532 regardless of the couple’s total. The community spouse’s own income is not restricted — they keep all income received in their own name.

What is a beneficiary deed in Arkansas and how does it protect my home from Medicaid?

An Arkansas beneficiary deed allows a property owner to name a beneficiary who automatically receives the real estate upon the owner’s death, without going through probate. Under Act 570 of 2021, the state may not file a Medicaid estate recovery claim against property transferred through a properly executed and recorded beneficiary deed. The owner retains full control and can revoke the deed at any time. The deed does not trigger the five-year Medicaid lookback period.

Why do I need a power of attorney for long-term care planning?

A durable power of attorney for finances allows a trusted person to manage your financial affairs if you become incapacitated — including applying for Medicaid, managing assets, and working with financial institutions. Without one, your family may have to petition an Arkansas court for guardianship or conservatorship, which is expensive and time-consuming. Every long-term care planning strategy requires someone with legal authority to act. A healthcare power of attorney is equally important for directing medical decisions.

What is the Arkansas Long-Term Care Partnership Program?

The Arkansas Long-Term Care Partnership Program links qualifying private long-term care insurance policies to Medicaid through a dollar-for-dollar asset disregard. For every dollar a Partnership-qualified LTC policy pays in benefits, Medicaid will protect that same amount of assets if you later need to apply — even after your insurance benefits are exhausted. The protection also applies to Medicaid estate recovery after death. Partnership policies must include age-appropriate inflation protection and meet requirements of the Arkansas Insurance Department.

—

This post is intended for general informational purposes only and does not constitute legal advice. Reading this post does not create an attorney-client relationship between you and Winburn, Case, Schrader & Shram, PLLC. Every situation is different, and the law as it applies to your specific circumstances may differ from what is described here. If you have questions about your estate plan or any legal matter, we encourage you to consult with a qualified attorney.